5 tips for managing foreign currency risk in international markets

Companies work to put COVID behind them and forge ahead with global expansion

3 min read

COVID-19 changed nearly everything about how businesses operate. But has it changed where?

Early in the pandemic, experts predicted that global expansion would come to a screeching halt—that travel restrictions and supply chain delays would thwart all growth plans. But recent data from Middle Market Growth tells a different story.

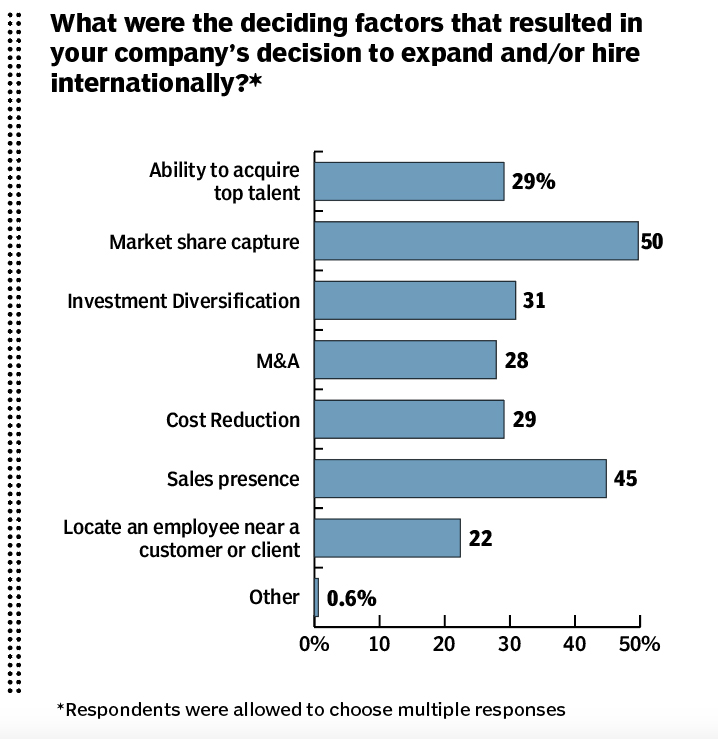

The survey of 166 CFOs and other senior finance executives found that only 37% have halted their expansion plans because of COVID. Another 45% said there were either expanding globally or only slightly delaying their plans within the next year. Another 9% intend to expand in one year or more.

But the finance chiefs also have worries about global markets in a volatile economy. Some 83% expressed concern about dealing with third parties and stakeholders in a foreign country; 74% worried about dealing with foreign banks and international employee payrolls; and one in 10 agreed that tax compliance demands posed a barrier.

With a troubling economic year in the rearview mirror, many companies are forging ahead, said David Maher, manager of international sales and trading for BOK Financial®.

Source: www.cfo.com

“The economy is global. It’s not national anymore. A lot of major corporations derive 45-50% of their earnings or better overseas. More and more, we’re seeing companies grow into international markets.”- David Maher, manager of international sales and trading

“The economy is global,” he said. “It’s not national anymore. A lot of major corporations derive 45-50% of their earnings or better overseas. More and more, we’re seeing companies grow into international markets.”

For companies looking to expand internationally, Maher offers these five tips:

-

Hedge currencies. Fluctuation can impact profit margins or costs, so it’s beneficial to lock in prices. This can be done through forward contracts—locking in an exchange rate on a future contract.

“Known results are always preferred to unknown,” Maher said. “For example, you may not know how exchange rates are going to fluctuate, so lock in everything you can. If you have an invoice that’s 90 days out, you can lock in the rate at the date of invoice, rather than the date of pay to ensure you don’t lose money in the process.”

-

Price locally. “Make it easier for acquiring customers to purchase from you,” he suggests. Pricing goods and services in the customers’ currency helps you compete with local competition. “If you let someone else price it for you, they’re going to put on a big premium and you’re probably going to lose business. Don’t let the market set your prices.”

-

Know your market. Be aware of what influences the currencies you’re exposed to—such as commodities, politics and regulations. A wide range of factors can affect currency exchange rates, including new governmental administrations, weather, supply chain interruptions, workforce education and labor, interest rates, and inflation.

“Know what’s going on with your target demographic,” Maher said. “Keep an eye on news for that country, especially government and economy news, and spend time reading trade and industry publications. Essentially, be engaged with the market.”

-

Dual invoice. When making an international purchase, make it a simple financial equation. More often than not, this will result in savings to the bottom line.

“We recommend invoicing in local currency and the U.S. dollar,” he said. “For example, if you get two invoices, you’ll have the price in Euros and the price in dollars and you can see which is cheaper. Based on that information, you can then send a currency wire rather than a dollar wire, and there’s no other difference.”

-

Know the rules of withdrawals. Making deposits is easy, but documentation and protocol around withdrawals differ from country to country.

“If you’re looking at growing your business overseas for the first time, prepare to create and utilize a different financial strategy,” Maher said. “Hope is not a strategy. It’s important to have a plan that is specific to the country.”

It’s a lot to navigate. Every country is different, and every country is ever-changing, Maher said.

“The informed mind has an advantage, as they say, so it’s important to build relationships with your financial partners who are experienced navigating these variables,” he said. “Ask all the questions and stay engaged.”