Resurrecting your short game

Effective portfolio management once again includes short-term holdings

The long-sleepy corners of investor portfolios where cash and short-term investments live have experienced a renewed vibrancy over the past year or so.

The resulting opportunities have proven increasingly enticing to wealthy investors who realized they didn't have to settle for next-to-nothing returns on their large cash balances anymore. Higher-yielding savings accounts, certificates of deposit (CDs), Treasury bills and money market funds have become viable components of investors' portfolios.

However, experts note that, as with any asset class, today's juicy returns on short-term investments could sour quickly, especially if they distract from potentially better opportunities elsewhere.

Higher rates stoke renewed interest

The resurgence in short-term investments emerged from the aggressive anti-inflation campaign the Federal Reserve launched in March 2022. By swiftly raising its key lending rate to 5.0% from essentially zero over a 15-month period, the Fed helped reawaken the prospects of meaningful short-term investment returns distinct from stocks and longer-term bonds, where valuations tumbled (and yields soared) in 2022.

"The speed of the hikes caught many by surprise and people who haven't looked at their short-term holdings in something like 15 years found themselves playing catchup, no doubt about it," said Greg Wheeler, director of private wealth for BOK Financial®. "Previously, when cash was earning nearly nothing and it was just essentially stored by money market mutual funds and financial institutions, there wasn't much value in developing a cash strategy.

"Today, however, with cash rates elevated and a growing likelihood that those rates will return to traditional levels sooner rather than later, a thoughtful cash plan is essential."

Safety enhancements

Overall, Wheeler said the short-term investment landscape remains investor friendly as banks and other financial service firms have ramped up the competition for deposits.

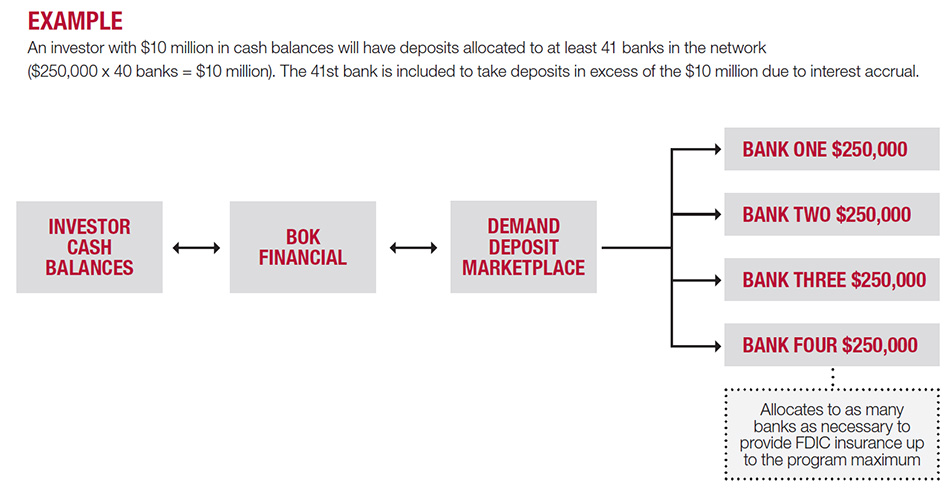

Bank offerings include an added element of security as holdings worth up to $250,000 are guaranteed by the Federal Deposit Insurance Corporation (FDIC)*. Specifically for large depositors, Wheeler said bankers may coordinate FDIC protection into the millions of dollars by working through one of two intra-bank services:

- Insured Cash Sweep, which distributes cash in up to $250,000 increments in checking and money market accounts across banks that belong to the IntraFi Network.

- The Certificate of Deposit (CD) Account Registry Service, which taps the IntraFi Network for CD investments that also fit under the FDIC umbrella.

"By spreading the money around to other banks, both approaches offer competitive returns but resolve concerns large depositors may have with safety," he said. "That said, it's important to work with a bank you can trust to ensure optimal returns and safety."

Wheeler added that cash-return-minded investors may also invest directly in U.S. Treasury offerings, which are considered risk-free but can be challenging to navigate for individuals, and money market accounts, which tend to offer lower yields. Management fees may also detract from returns on both approaches.

"You can try to manage your short-term portfolio yourself, but it's not very efficient, especially for large amounts of cash," he said.

Rate increases likely close to done

An investment portfolio's cash position provides liquidity in exchange for relatively modest returns, Wheeler said. Such accounts are typically used to hold emergency funds for an individual or business but may also provide a temporary home to proceeds from the sale of stocks or other assets.

When yields on bond investments ranging from seven-day Treasury bills to one-year Treasury notes started climbing higher than long-term yields in early 2022, investors started reassessing their liquidity needs with the chance to improve their portfolio's short-term cash flow. Those considerations have grown even more pointed as Fed officials have started to hint that their rate-hike campaign may soon be coming to a close.

“We're having conversations with clients on a regular basis to determine their sleep factor—how can their portfolio be structured so that they sleep at night. That includes looking ahead to when the yield curve un-inverts and short-term interest rates fall back below long-term rates”- Greg Wheeler, director of private wealth for BOK Financial

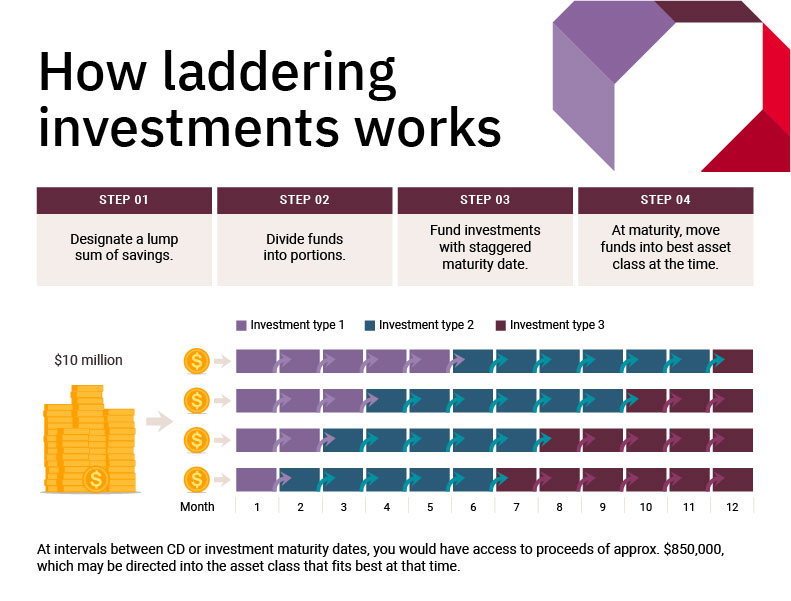

To buffer the potential fallout from any decline in short-term rates, Wheeler suggests a laddered approach in which a total investment is spread evenly across a desired time frame. As each portion matures, the investor may direct the proceeds into the asset class that fits best at that time.

"You cover your bases, especially as the yield curve un-inverts," he said. "Maybe the stock market is picking back up or you want to get into a longer-term bond or buy municipal bonds—essentially things you might want to invest in other than just cash."

For example, an individual looking to invest $10 million on a short-term basis over the next 12 months may ladder their holdings so they get a bit under $850,000 back every month to deploy as they best see fit.

This approach to global asset allocation planning identifies where assets are and how they may accommodate any shortcomings or issues that occur. Short-term investments follow the same rules as all other asset classes in terms of diversification and the principles of bond investing, Wheeler said.

"You don't invest everything in the front end and you don't put everything in the back end," he said. "You spread it out based on when you'll need that cash and where you can take the risk."

Contact our Private Wealth team for more information.

*The Federal Deposit Insurance Corporation (FDIC) is a US government corporation that insures the money in your accounts up to $250,000. Our CDs, checking accounts, savings accounts, and money market accounts are insured up to the maximum $250,000 per depositor, as allowed by law.