Why 30-year mortgage rates hit a new year-to-date high

Investors are rethinking how quickly the Fed may reach its 2% target for inflation

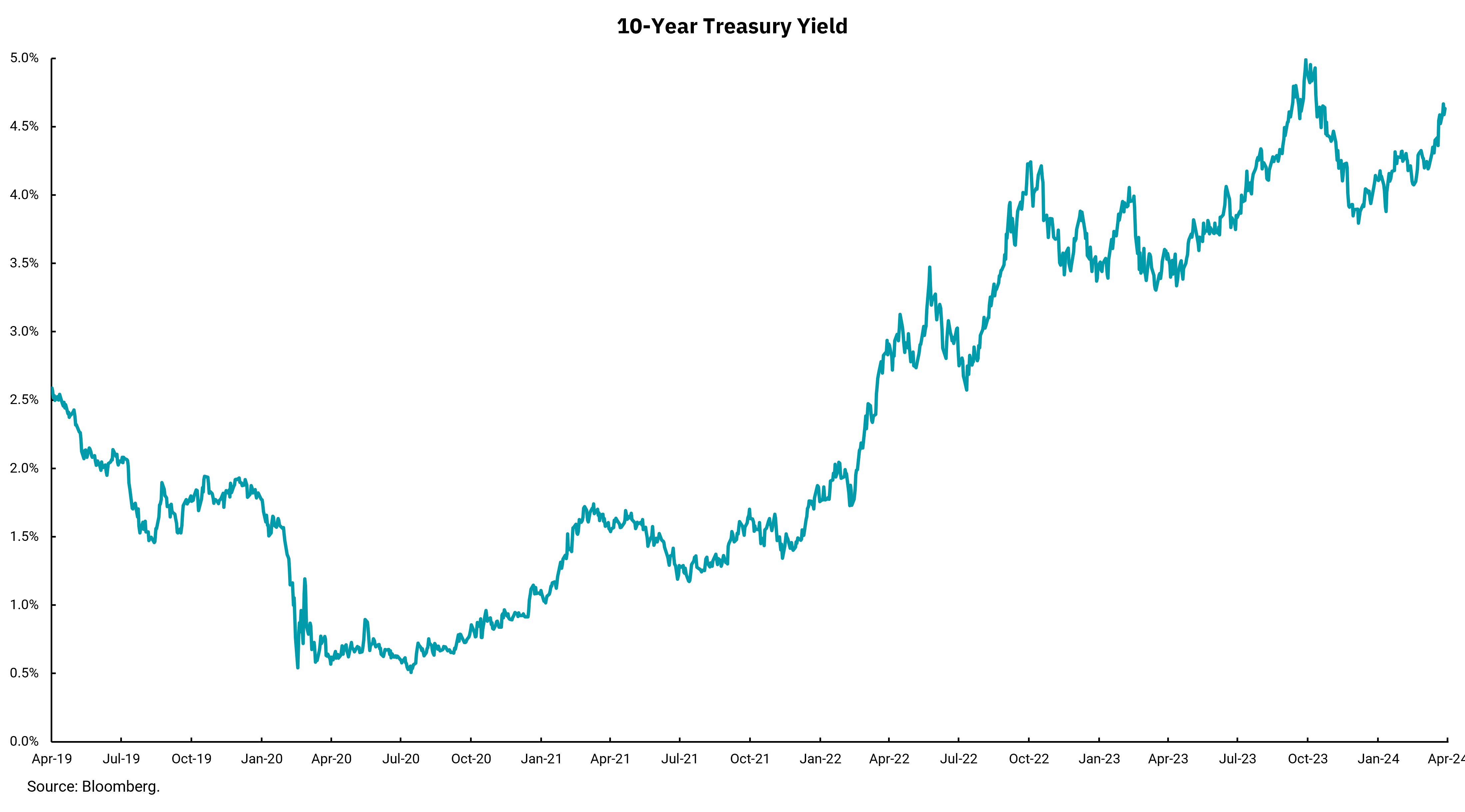

Few interest rates are as important to the global economy as the U.S. Treasury 10- year note. In addition to being a bellwether rate that signals how the overall economy is doing, it serves as the basis for pricing popular 30-year home mortgages. Mortgage rates don’t move in tandem with the 10-year Treasury because the spread between the two can change; however, the direction of rate moves is most often the same.

Interestingly, unlike shorter-term rates like the overnight Federal Funds rate, the Fed does not directly control longer-term rates like the 10-year. Where and in which direction shorter-term rates are moving can be a big influence. Still, the 10-year rate is influenced more heavily by factors like longer-term inflation expectations and U.S. and global economic growth projections. This explains why there are times, like now, when the 10-year rate is below shorter-term rates, like Treasury bills and the two-year Treasury note. These periods of “inverted” rates are a strong indicator that the market is anticipating inflation to fall over time and that the Fed will be able to lower shorter term rates below those on longer maturity notes and bonds.

Our chart this week covers 10-year Treasury yields five years back to April 2019, before the onset of the pandemic. Recall that, before the pandemic, we were in the midst of a long period of very low short-term rates as the economy progressed in its long, slow recovery from the Great Recession, and inflation remained at or below the Fed’s 2% target. When combined with the Fed’s program of quantitative easing, where they were expanding their balance sheet by buying Treasuries and mortgage-backed securities, the 10-year rate and 30-year mortgage rates remained low. The onset of the pandemic only exacerbated the decline in overall rates. The quick recovery, however, aided by generous amounts of fiscal policy support from Congress, led to increasing inflation rates. In response, the Fed quickly increased overnight rates, which led to higher longer-term rates.

As the Fed has reached what we think is the peak in short-term rates, longer-term rates are moving more on the longer-term outlook again. After declining from their highs in November 2023, long-term rates have begun moving higher again as stubborn inflation is making it difficult for the Fed to start lowering their Fed Funds target and making investors re-think how quickly inflation might return to the 2% target. As 10-year rates have moved higher, 30-year mortgage rates have followed suit, recently hitting a new year-to-date high of near 7.5%.

Higher rates make all debt more expensive, but as we continue our progress forward from the pandemic, we will be watching longer term rates closely to try and discern what we might expect from inflation which, in turn, will help guide the Fed as they think about their next monetary policy move. Current rates reflect an outlook for continued economic growth, which is good but also might reflect a bit more stubborn inflation.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)