Housing and other core services prices still ‘stubborn'

With the ‘easy’ moves in inflation behind us, higher prices are likely to stick around

Inflation continues to be the biggest economic story for 2024. While it is true we have seen an "improvement" in inflation, we know this does not mean prices are falling; they are only going up more slowly. Additionally, while we also know the Federal Reserve considers "core" inflation more important from a monetary policy standpoint, most of us, as consumers and business owners, live in a "headline" inflation world.

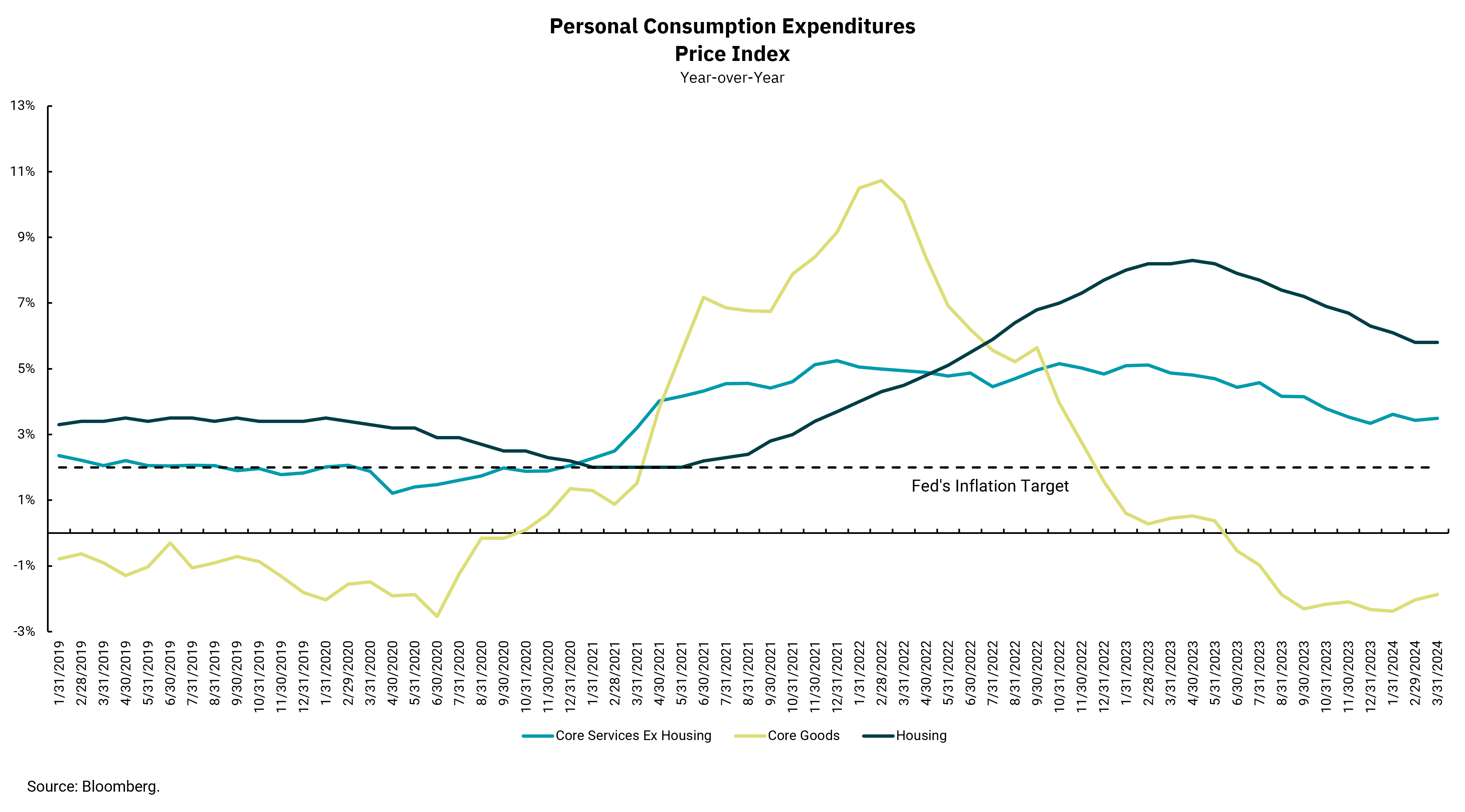

Recent inflation readings have shown that the path towards the Fed's 2% target might be a bit slower and more difficult than first thought. Among the different measures of inflation, the Personal Consumption Expenditures Price Index (PCE) is favored by the Fed. This week's chart digs into some of the components of PCE as we try to understand what happened with inflation during the pandemic and what that might mean going forward. Looking at inflation before the pandemic, we can see that "core goods" were a consistent source of disinflation. This was a positive result of the globalization of our economy. Since companies could seek out lower-cost producers, that helped keep goods prices low.

The impact of not only the pandemic itself but also the domestic policy response is clear in this week’s chart. Initially, as the government showered the economy with stimulus to avoid a long protracted economic decline, consumers could not spend the money as they had. Travel and restaurants were highly restricted, leading consumers to spend their money on goods— and we bought a lot of goods. However, China was pursuing zero-COVID policies which restricted goods production. Meanwhile, the goods that were produced got tangled in dysfunctional supply chains. The result was a massive increase in core goods prices.

Then, as we re-opened the global and domestic economy, consumers could spend money on more experiences, such as travel and eating out. At the same time, supply chains healed. Altogether, these encore goods back to a disinflationary path. However, as inflation surged, workers began demanding more pay, and an under-supplied labor market led to significant wage increases. Pandemic-period low mortgage rates increased demand for housing, which led to significant price increases in a supply-restricted market. In that chart, we can see these two areas were slower to respond to inflation but also slower to decline. In short, while the more cyclical areas of inflation are acting more "normal," the more secular parts of inflation—specifically, housing as well as core services excluding housing—remain a bit more stubborn.

Our sense is the Fed's next move will be to lower rates, but we must watch the more secular parts of inflation for clues on when the Fed might get more confidence in inflation moving sustainably to their 2% target. It seems the easy moves lower in inflation are behind us.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)