Despite tariffs and uncertainty, bond investors remain unruffled

Credit spreads not forecasting significant economic weakness

6 min read

There are numerous indicators we watch to try and divine the future of the economy. The Government, the Federal Reserve and private sources all produce a myriad of hard data sets that will follow trends in economic activity like inflation, growth, corporate earnings, retail sales, transportation, electricity usage— honestly, the list is very long. We also see soft data—for instance, surveys of consumers and businesses that attempt to measure how they "feel" about present and future conditions, along with their views on items like stock prices and inflation expectations.

The idea, of course, is to be able to look at some of these indicators to make decisions that will produce better outcomes than if purely left to chance—and we are not talking about just stock market investing decisions. Companies and individuals consider the broad mosaic of this information when thinking about capital expenditures. For example, companies may consider this information when deciding to build a new manufacturing facility, or individuals may consider it when determining whether to buy a house or a car. If only the breadth of the information we get could produce a clear picture.

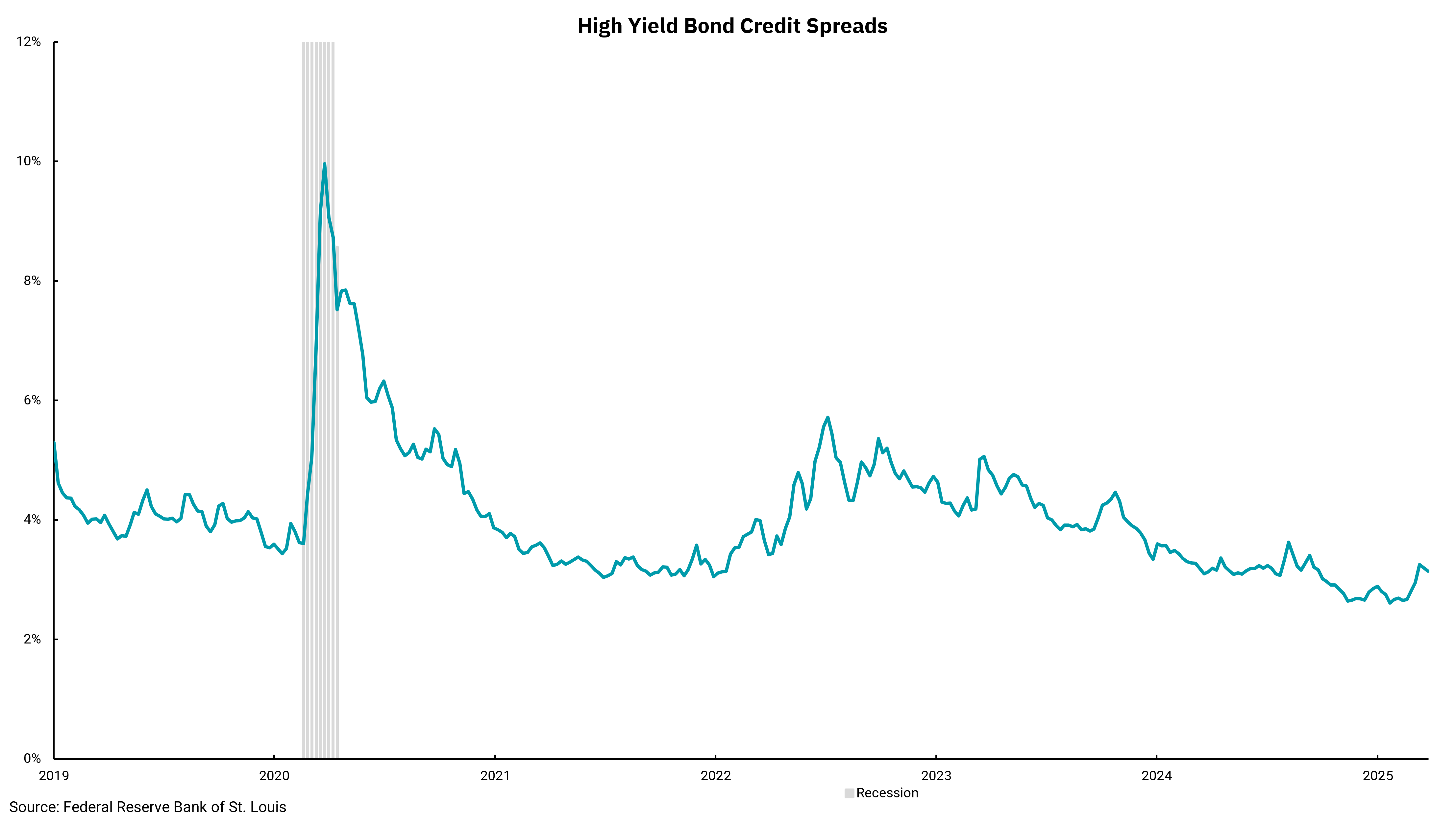

Our chart this week highlights one of the more important "market-related" indicators we follow: high-yield bond spreads. One of the biggest differences between bonds and stocks (and there are many of course) is the certainty of the growth rate on bonds. It is 0%. Simplistically, a bond is issued at par and, absent a credit event, matures at par, meaning the only way for a bond investor to make money is from the bond's stated coupon rate. This also means that, if bond investors want to make more money, they must demand a higher rate of interest. High-yield bonds should pay some additional interest rate over Treasuries to compensate a bond investor for the additional risk they are taking. Altogether, this means watching changes in the amount of spread demanded by investors can give us a strong idea of the bond market's view of the economy. If investors expect the economy to remain strong and companies to be able to service their debt, they will require a lower "spread" because the risk is less. If, however, investors expect a slower economy and the possibility of more defaults, they will require a higher spread because risk is deemed to be higher.

We can see this relationship between investors' economic expectations and credit spreads in this week's chart, as high-yield spreads widened dramatically during the pandemic-induced recession. When we consider that the National Bureau of Economic Research (NBER), the official arbiter of economic recessions, makes their assessment of whether a recession has occurred as they look back at their indicators, we can say the widening of credit spreads gave us a leading, or at least coincident, indicator of economic weakness. Thankfully, the chart shows that the credit markets are not forecasting significant economic weakness based on credit spreads today, but we are vigilant to see if recent stock market weakness spreads top the bond market.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)