Fed rate-cut debate intensifies

Mixed economic outlook continues, but slower growth likely

6 min read

The debate around rate cuts rages on. In July, the Federal Open Market Committee (FOMC) decided to keep rates the same, but two members dissented in favor of lower rates. Their dissent has added a more public debate element to an already mixed economic outlook. Internally, we have a varied set of opinions, and at this point, whatever decision is made will be cheered by some and pilloried by others.

There is always room for debate when considering monetary--and fiscal, for that matter-- policy. The dual mandate of the Fed, full employment and price stability, can often give conflicting signals, and such is the case today. There is even room for debate within each of the two pillars of their mandate. Inflation is below the current Fed Funds target, and the impacts from tariffs have been more limited than expected. However, the fact is that core Consumer Price Index (CPI) inflation is still over 3% and progress towards the 2% target has slowed. Recent Producer Price Index (PPI) data, along with surveys from purchasing managers and supply managers, show inflation pressures may be building within the overall economy. Tariff price pressures are generally deemed to be, dare I say it, transitory, but some level of increase in inflation indexes appears to still be in front of us.

Labor market data shows a headline unemployment rate of 4.2%, and weekly jobless claims continue to reflect an environment where companies seem hesitant to reduce employee headcount. At the same time, data within the Job Opening and Labor Turnover Survey (JOLTS) and continuing claims also confirm that the rate of hiring has slowed. Recent college graduate unemployment rates are elevated.

Within each of these two mandates, one can build a credible case for stable or lower rates. Few economists at this point are forecasting an outright recession, but a period of slower growth is evident. Slower growth and sticky inflation has a “stagflationary” feel to it.

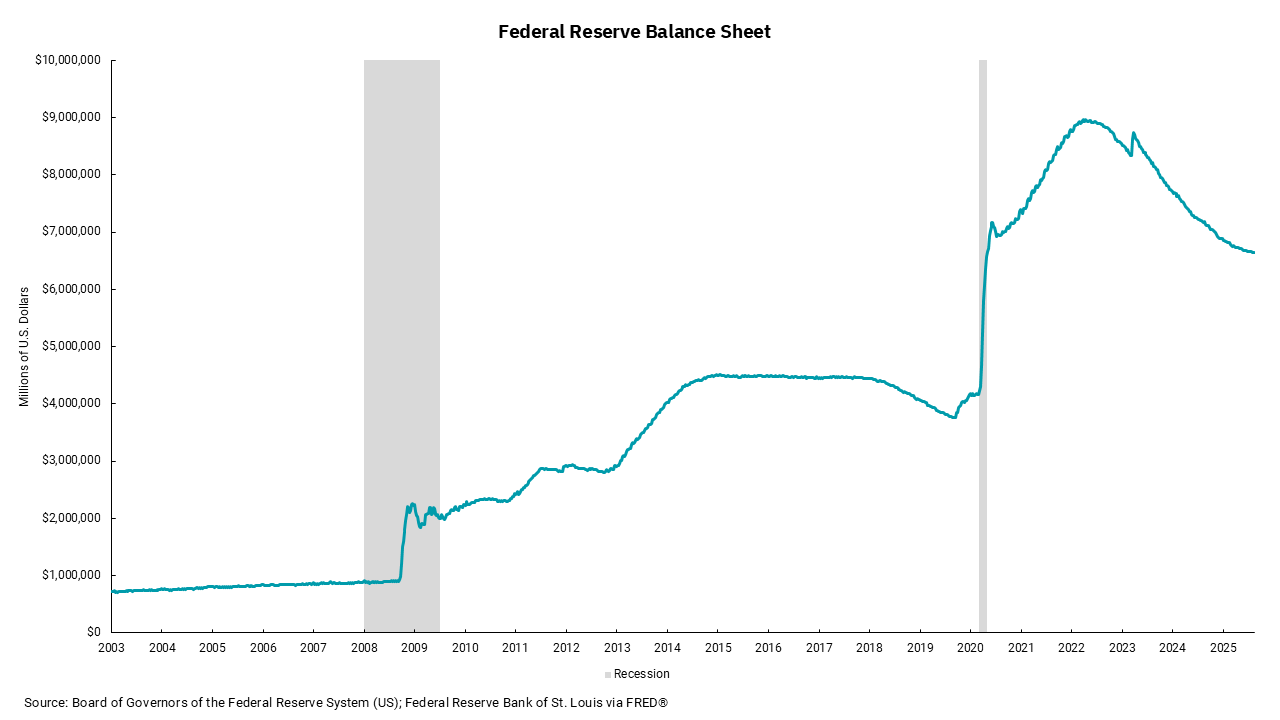

The other aspect of the Fed’s current monetary policy stance, which is not getting as much attention as rates, is its ongoing policy to shrink the size of its balance sheet, known as quantitative tightening. This part of monetary policy does not have the immediate or visible impact as rate decisions. Still, it can be just as important as we think about the capital markets and even consumer rates like home mortgages. Since the Fed started reducing the size of its mortgage holdings, overall mortgage lending spreads have widened, leading to somewhat higher borrowing rates for prospective homeowners. It also matters what part of the yield curve in which the Fed is active. As borrowing by the Treasury heats up based on the recent debt ceiling increase and the need to refill the Treasury General Account (TGA), the Fed could be an influence based on its decision on how to reinvest maturities and interest payments. In short, this is all about managing the supply and demand balance between the issuer, the U.S. Treasury and investors. A mismatch could lead to market imbalances which could be disruptive across multiple sectors of the capital markets.

Fed Chair Powell’s speech on Friday could have some longer-term implications based on how he communicates what the Fed is thinking. Then again, this is his last speech at this event as Fed Chair, and we cannot ignore that future Fed Chairs might feel differently about the path we should be on.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)