Fed rate cut signals broader growth ahead

Earnings gains expected to broaden beyond AI-driven stocks

6 min read

KEY POINTS

- The Fed’s latest rate cut reflects concerns about labor market weakness and inflation, setting the stage for gradual policy shifts in 2026.

- Market optimism is fueled by forecasts of broader earnings growth beyond the Mag 7 and into small-cap stocks next year.

- A diversified investment approach remains key as economic acceleration and sector rotation reshape market dynamics in 2026.

The Federal Reserve’s interest rate-setting arm, the Federal Open Market Committee (FOMC), met last week and decided to lower interest rates by another 0.25%. It was the third meeting in a row where the decision was to cut rates. However, as has been the case recently, there were multiple dissents to the action: two dissents were in favor of no rate cut, and one was in favor of a 0.5% cut. It is increasingly clear that the range of opinions among FOMC members is wider than in recent periods, all while Fed Chair Jay Powell’s tenure as the Fed Chairman is winding down. This seems to be allowing an environment where differing opinions are more comfortably expressed.

The primary motivation for the cut was a sense that the labor market has weakened over the past few months and that unemployment may move higher, which would put the U.S. consumer at risk from an overall economic growth standpoint. At the same time, inflation remains above the Fed’s target, leading some FOMC members to be concerned about lowering rates too much and slowing, or even stopping, the progress towards the Fed’s 2% inflation target. Additionally, in post-meeting comments, the Fed acknowledged the ongoing stress on lower-income consumers from aggregate inflation over the last few years. The term being widely used in the press is “affordability”.

The markets’ reaction was broadly positive. Short-term rates fell more than long-term rates as the yield curve steepened further, while stock markets saw price gains. Our outlook is for limited cuts going into next year, so the bond market might be a bit more stable after seeing broad-based positive total returns this year. For stock markets, there are a couple of factors that lead us to remain optimistic and stay diversified in our approach.

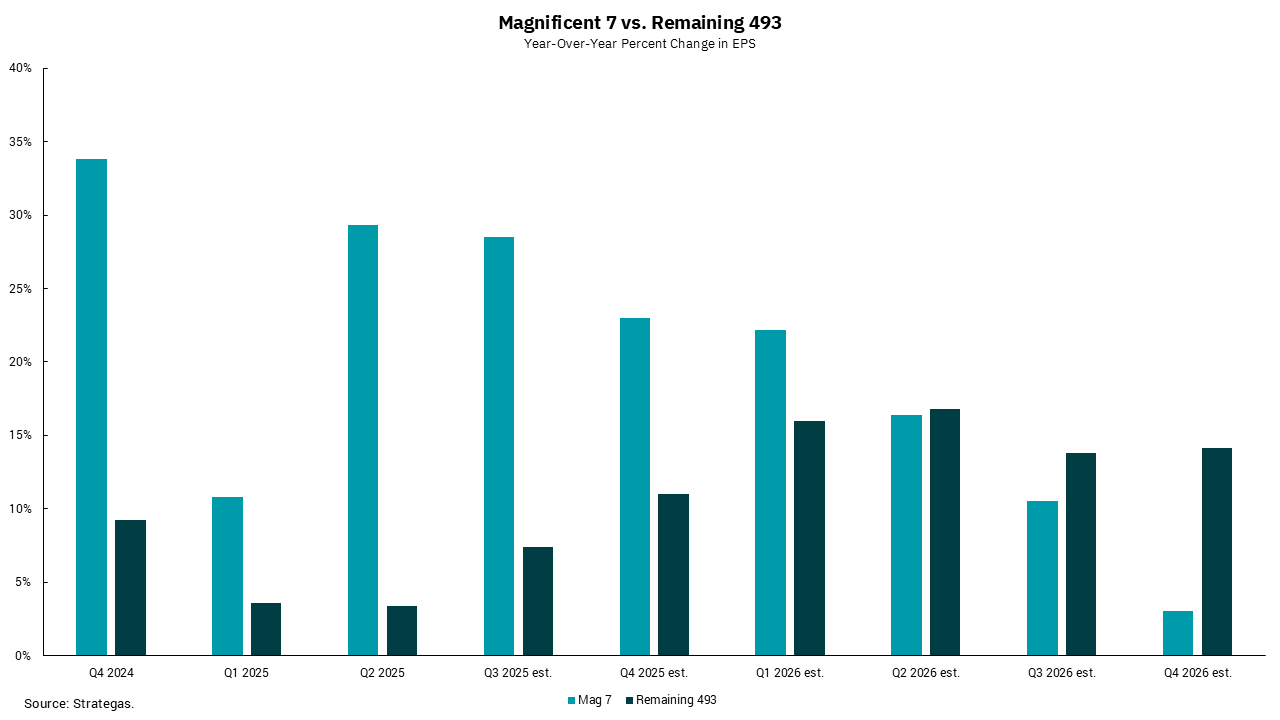

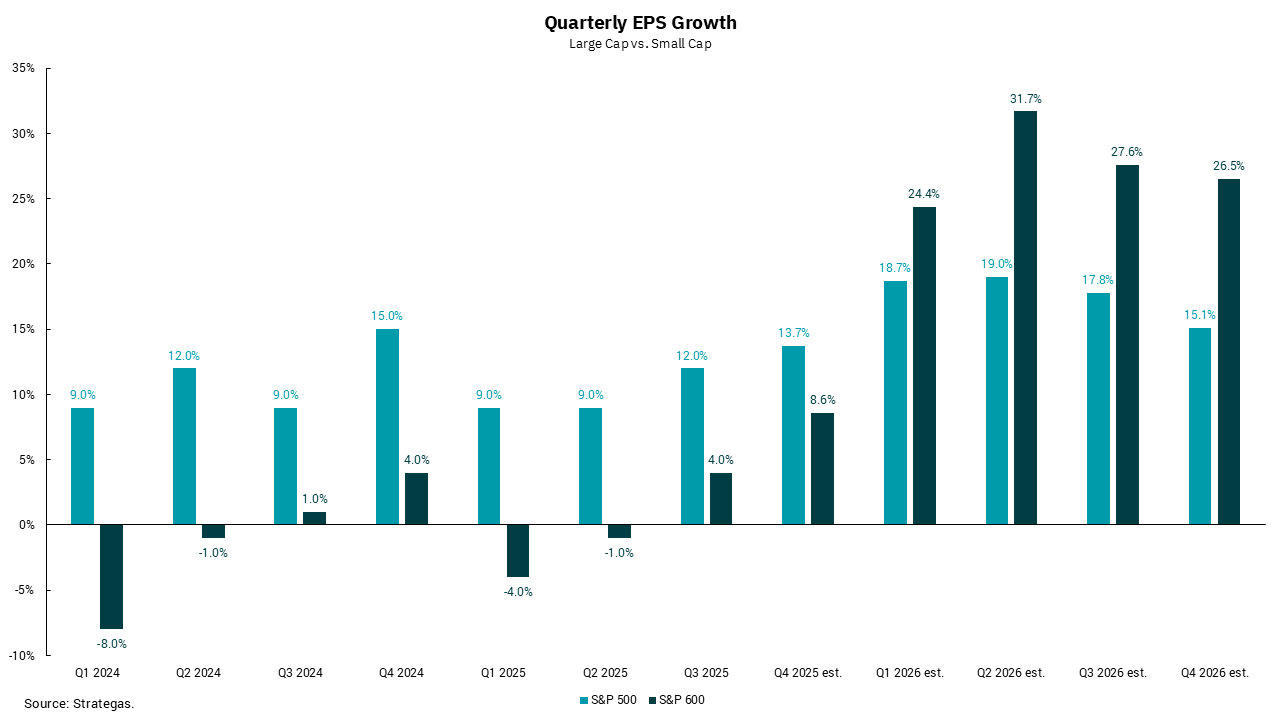

The top chart shows a look at earnings estimates for the Mag 7 versus the S&P “493” (the non-Mag 7 stocks in the S&P 500), while the bottom chart looks at earnings growth estimates for small-cap stocks (S&P 600) versus large-cap (S&P 500). In both instances, we are seeing a shift from what has driven the market over recent quarters. Within the large-cap space, we anticipate earnings growth for the S&P 493 to outpace that of the Mag 7 by the second quarter of 2026. Looking at small-cap versus large-cap, we anticipate small-cap earnings outpacing large-cap earnings beginning in the first quarter of 2026.

Both of these factors reflect an economy expected to accelerate next year and broaden to include more than just the AI-driven stock performance of 2025. This does not mean the AI trade is over; it just means growth rates for those companies will slow, and as the economy broadens, other sectors and market caps will participate. We remain committed to our diversified approach to equity portfolio construction.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)