The most important price in capital markets isn’t a stock

Why a non-politicized Fed matters to bond investors

6 min read

KEY POINTS

- Credit spreads and weekly jobless claims remain key indicators for validating or challenging the positive growth narrative.

- Geopolitical tensions and shifts toward a multipolar world present meaningful risks that could disrupt the base case outlook.

- Historically, positive January performance corporate incentives could fuel spending and investment, driving growth in 2026.

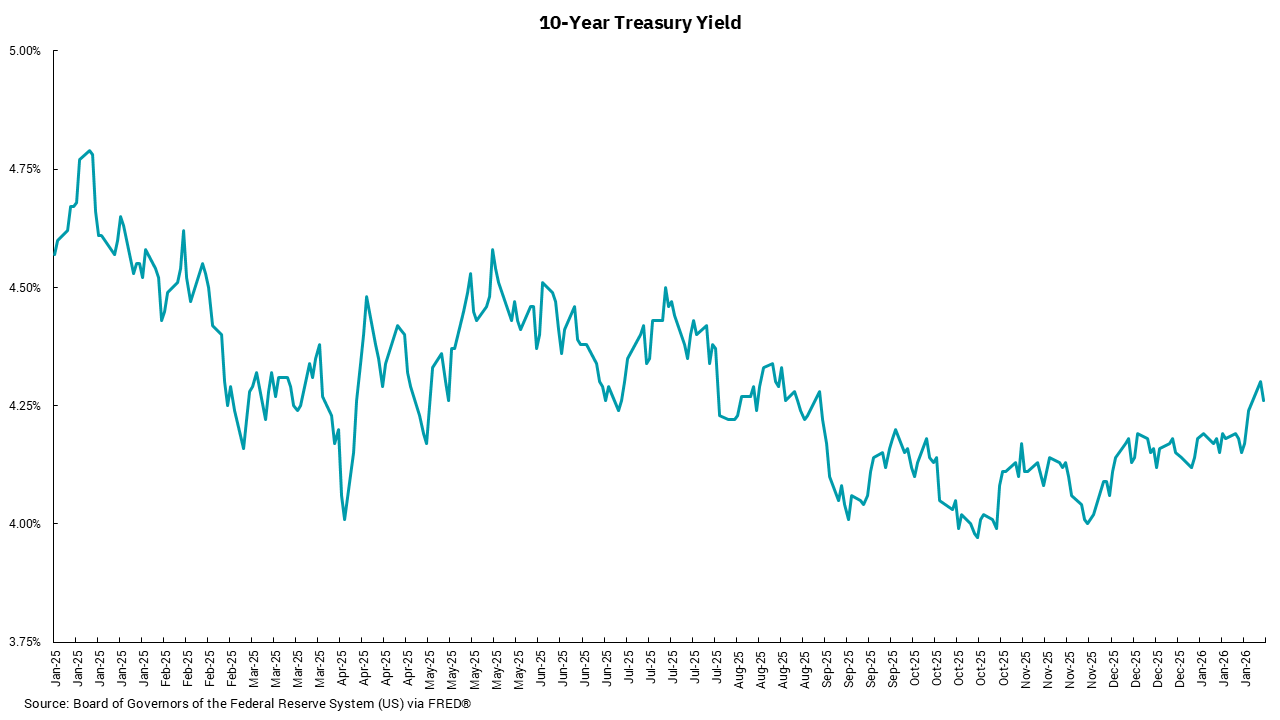

The most important “price” in the capital markets is not NVDA or GOOG or MSFT or META— although those prices are important. No, it is the 10-year Treasury note yield. Yes, the entire rate structure matters. The shape of the yield curve matters. Credit spreads matter (a lot). However, there is no single more important variable in the valuation process of the capital markets than the 10-year Treasury note. In short, it serves as the valuation basis for all markets —public, private, bond and equity.

While there are a multitude of ways to measure a market’s, or a single security’s, “value”, the overarching idea is to take future cash flows, known in the case of a bond and unknown in the case of an equity, and discount them back to a net present value (NPV). This discounted NPV then serves as the decision point for investors to buy or sell, based on their known or assumed idea of the future. Assumptions, of course, introduce the possibilities of varying opinions and help make the idea of a market work. For every willing buyer at a given price, there needs to be a willing seller. Yet the most important assumption or variable in the NPV calculation is not the level of future cash flows, but the rate at which those future assumptions are “discounted” back to derive the NPV. Here is where the 10-year Treasury comes into play.

For many, but not all, the idea of the “risk-free” rate of return is defined as the rate on the 10-year Treasury note. For investors, it is the rate that they can earn without taking any “risk” as U.S. Treasuries are deemed to be free of any credit risk. (Yes, I know there might be a few smirks on faces considering that U.S. Treasuries are no longer Aaa/AAA rated, but we are where we are.) This mean that if an investor is going to buy a security with risk, they will need to generate a return higher than this amount to make it worthwhile. In the “math” of valuation, then, a higher “risk-free rate,” or discount rate, results in a LOWER NPV. A lower “risk-free rate” results in a HIGHER NPV. That is why, in general, the capital markets like lower rates and not higher rates.

This concept takes on added importance as we think about what is going on at the Federal Reserve now. If we focus solely on the fundamentals of inflation, our view is that we should continue to see a moderation towards the Fed’s stated target of 2%—albeit, slow progress. Within that environment, it would be reasonable to expect longer-term rates to trend a bit lower.

However, the introduction of the idea of a politicized Fed might overwhelm the shorter-term fundamentals and lead to the longer end of the Treasury curve, including the 10-year Treasury, to go higher in yield as investors price in a higher risk of the Fed making decisions that are not based upon keeping inflation low for the longer term. We DO NOT think the U.S. is in that position yet, but it is a risk we must monitor more closely now than we have in a very long time. The Fed’s credibility rests on its ability to maintain price stability, even if that is at odds with its other mandate of full employment. Bondholders will not take kindly to seeing Fed actions outside their best interests.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)