The job market isn’t cracking; it’s normalizing

Steadier growth may be ahead, even as layoffs rise

6 min read

KEY POINTS

- Weekly jobless claims and unemployment data suggest a stabilizing, not weakening, labor market.

- The Fed has paused rate cuts as growth expectations improve and recession risks decline.

- Despite soft spots, current trends point toward ongoing economic normalization rather than deterioration.

The health of the labor market is at, or very near, the top of factors we consider as we think about economic growth, earnings, the stock market, the bond market and Federal Reserve monetary policy going forward. Rightfully so, as full employment, along with price stability, make up the two pillars of the Fed’s interest rate policy framework.

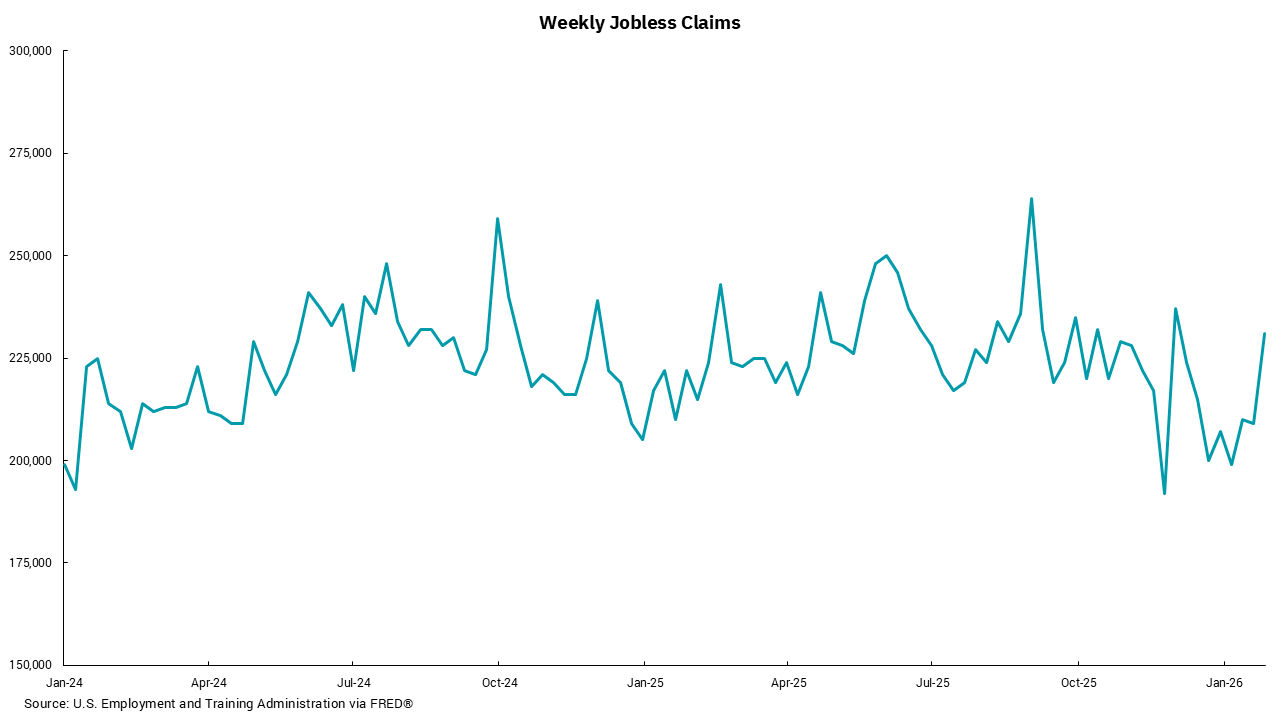

After lowering rates for three meetings in a row in 2025, the Fed paused at its recent January meeting. With inflation measures still above the Fed’s 2% target, the basis for lowering the overnight rate was growing signs of potential labor-market weakness. In the fourth quarter of 2025, we saw headline unemployment rise as high as 4.6%, and the general consensus was that the government shutdown, which became the longest in U.S. history, would slow growth and potentially exacerbate the increase in unemployment. Instead, we saw measures like weekly jobless claims, as shown in our chart this week, decline, and the headline unemployment rate now stands at 4.4%. At the conclusion of the most recent FOMC meeting, Fed Chair Powell highlighted some changes in how the Fed views the next few months. The Fed raised its outlook for growth and reduced its assessment of the risk of unemployment increasing.

Regular readers know that we are optimistic that economic growth will increase and, despite recent equity market volatility, we think stock prices will rise over the course of the year. Yet we also know divining the future of our economy and markets is exceedingly difficult. The recent “mini government shutdown” postponed the scheduled release of the January employment report until next week. However, we still have private measures of employment, the Job Openings and Labor Turnover Survey (JOLTS) and the weekly jobless claims. Taken in aggregate, the readings tend to show that the current “low firing/low hiring” environment persists.

However, there are potential trends that we need to watch closely. Layoff announcements have increased, open jobs continue to fall, the weekly jobless claims number increased and continuing unemployment claims remain elevated. That said, looking longer term, this may be considered a continued “normalization” of the job market, not an outright weakening trend. Looking at the last two years of jobless claims gives some idea of what we are talking about. While there was a recent jump in jobless claims, they have been at higher levels over the last two years without tripping the U.S. into a significant slowdown or recession. Where we would become more concerned is if the four-week moving average started to approach the 250,000 level. Jobless claims have hit that level a few times over the last two years, but then receded, keeping the four-week average below that level.

We don’t foresee the January employment report to be strong, but we also remain optimistic that the outlook for growth will keep headline unemployment supportive of the U.S. consumer going forward.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)