GDP slipped in 4Q but look for stronger growth ahead

Fed likely to cut rates once, maybe twice, this year

6 min read

KEY POINTS

- Fourth‑quarter GDP growth slowed sharply as government spending cuts from the prolonged shutdown weighed on the economy.

- Consumer spending softened but is poised to rebound with higher tax refunds and a steady job market.

- Strong capital investment supports a firmer growth outlook despite sticky inflation.

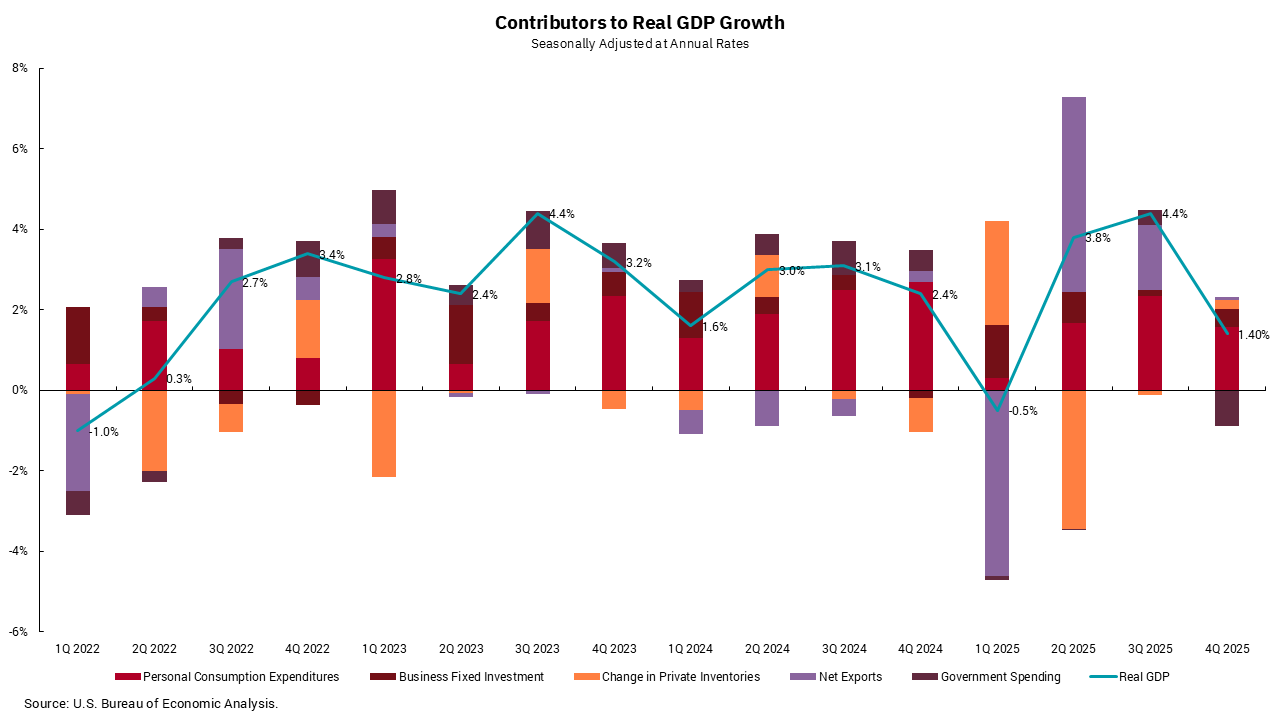

Reports on gross domestic product (GDP) growth are among the most delayed data points. The complexity of our economy makes it hard to get a read on anything resembling a “real-time” basis. The Atlanta Fed publishes a “GDPNow” model estimate, which attempts to provide a timelier look at growth, but the first official look at fourth quarter 2025 GDP from the U.S. Bureau of Economic Analysis (BEA) showed a reading of 1.4%, versus the “GDPNow” estimate of 3%, indicating how difficult modeling our economy might be. The GDP data is subject to further revisions in the weeks ahead.

Thinking broadly, it is not surprising that growth in the fourth quarter slowed from the longest government shutdown in U.S. history. We see this reflected directly in the data, as government spending reduced growth by 0.9%. Not unlike the variability in GDP from trade in the first half of this year, the decline in government spending might rebound and be a source of growth in the first quarter of 2026. It should be noted that attempts to rein in government spending as part of a budget process will be a headwind to this economic growth measure, even though this might be something needed over the longer term.

Personal consumption expenditures remained positive but came in a bit lower than they were in the third quarter. This could reflect some level of weakness in the job market or a bit of reduced confidence from the shutdown; however, here, too, we expect a rebound in the first quarter, driven by higher tax refunds and job market stability. Recent capital expenditure plans from the artificial intelligence (AI) hyperscalers and an increasingly broad array of other companies lead us to be a bit more confident in growth from businesses fixed investment, another tailwind to growth for 2026.

We also got a reading on the Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures Price Index (PCE). Looking at the more important “core” inflation reading, which excludes volatile food and energy, the number was reported at 0.4%, versus expectations of 0.3%. This brought the year-over-year rate to 3%, versus expectations of 2.9%. This reading is not enough to materially alter our shorter-term outlook for the Fed, but it does show that progress towards the Fed’s 2% inflation target remains a work in progress. Our outlook is for one, maybe two, rate cuts this year as inflation remains a bit sticky, and growth moves up from here. Improvements in productivity will limit the risk of inflation accelerating, but consumers will still feel the pinch of higher aggregate prices. This factor was reflected in the negative spread between wage growth and consumer spending, which pulled the overall savings rate down to the lowest level since 2022. Still, we remain more optimistic than pessimistic looking forward.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)