Relief may come for the pain at the gas pump

The conflict in Iran has pushed oil prices higher, but the pressure may not last

KEY POINTS

- Oil prices for immediate delivery have surged, while prices for future delivery have risen much less, suggesting markets expect prices to come back down.

- How long energy prices stay high matters more than how high they go when it comes to inflation and household budgets.

- The U.S. may feel less impact than other regions, since global supply disruptions affect overseas oil markets more than domestic production.

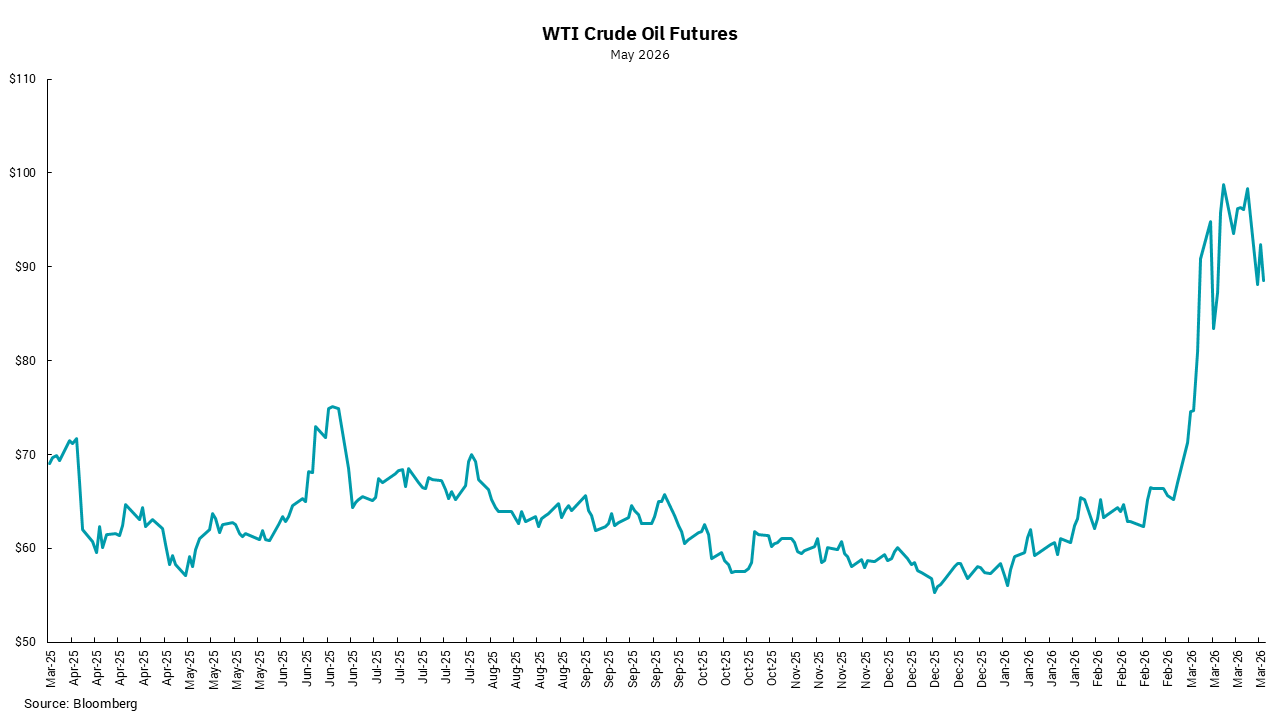

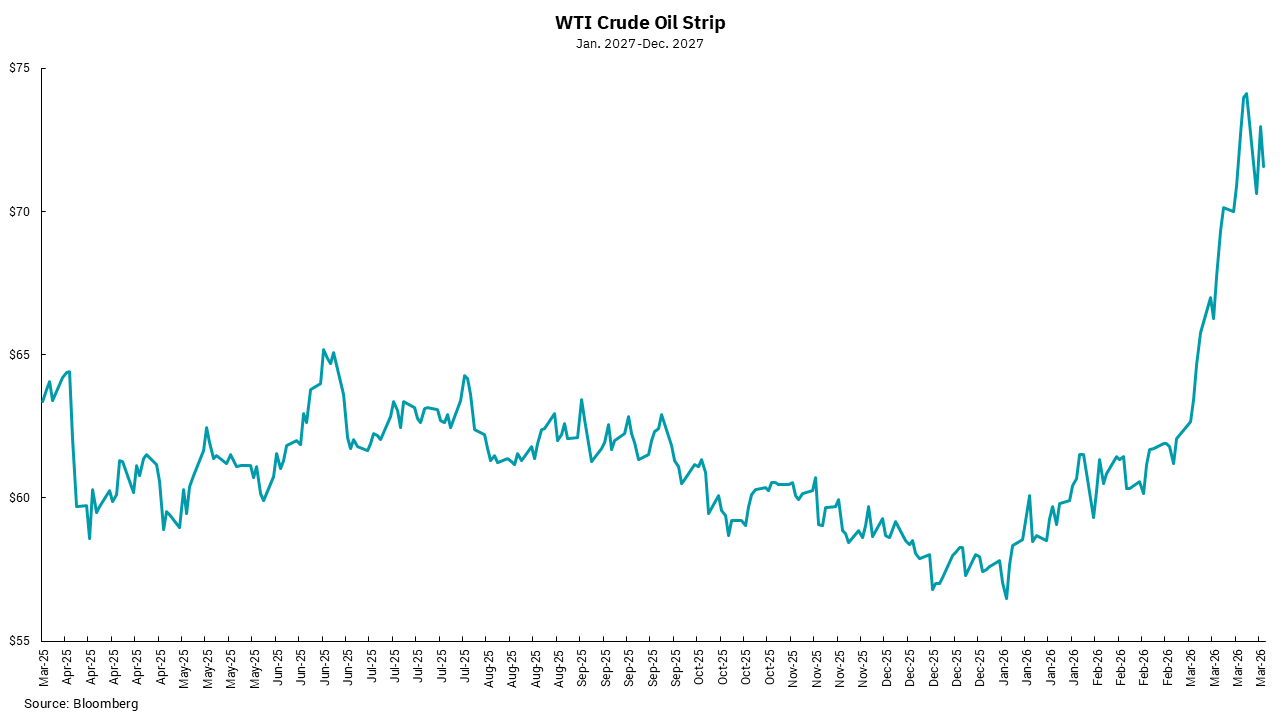

The conflict in Iran has introduced a new level of uncertainty in the domestic economy and spurred oil prices to much higher levels. In general, higher energy costs will squeeze consumers still struggling with the impact of aggregate inflation from the pandemic and, over time, will lead to higher overall prices as everything from production to distribution is touched by energy costs. No one knows for sure how long the conflict will last, but we can get some clues about the potential impact to energy costs from oil markets. Specifically, we can get these clues by comparing the price movements in the “spot” market to the prices for longer-dated futures delivery of oil. Our two charts this week show this.

The top chart is the “spot” or immediate delivery market, while the bottom chart is the average price for oil to be delivered in 2027. The direction of the move since the start of the conflict is the same, higher. However, the magnitude of the moves is not. Note the spot price at the beginning of the conflict was between $65 and $66 per barrel. At the same time, the average price for delivery in 2027 was just a bit lower at roughly $62.50 per barrel. Since the conflict began, though, the spot price increased to a high of $115 per barrel before settling back to around $92 per barrel as of this writing. This represents a 40% increase. The average price for 2027 went from $62.50 per barrel to a high of around $76 per barrel before settling back to about $72 per barrel. This represents an increase of only 21%.

What might we draw from this? It would seem oil traders are expecting lower overall prices as this conflict will eventually be settled and prices decline. For U.S. consumers, that outcome would be good news as we should see prices for products like gasoline, diesel and jet fuel begin to fall, removing some of the stress people are now feeling. As we think about the impact to the economy from higher energy, it is not just how high prices go but for how long they stay higher. On that front, it is the movement in the longer-term price for oil that is more impactful. If the longer-term average price continues to move higher, traders would be showing the greater risk of an extended conflict or broadening conflict that results in material damage to the infrastructure needed to produce and distribute oil. In that case, we would expect consumers to react by spending less on other items and the Fed would be in a difficult position as demand slows while inflation pressures rise.

Another important note: these charts are for West Texas Intermediate (WTI) crude oil, which is based domestically. The “other” oil price we follow is Brent crude oil. There is normally a difference between the two, with Brent usually trading a bit higher than WTI. It is possible we could see this spread between WTI and Brent widen in the future. Why? The U.S. is basically self-sufficient from an oil standpoint between domestic production and the now growing imports from Venezuela. The Iran conflict therefore is having a bigger impact on Brent oil buyers. Before the conflict, 80% of Iran’s oil production was being sold to China and, overall, nearly 20% of the world’s daily oil supply travels through the now effectively shut-down Strait of Hormuz. Extending or broadening conflict thus could lead to greater supply disruptions for the Brent market than for the WTI market.

The bottom line, however, is that while the conflict is not good for anyone, and we all hope for a quick resolution, the potential impacts might be less for the U.S. than the rest of the world.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)