Why we’re more optimistic than pessimistic

Economic growth, AI‑driven capital spending and steady job markets support positive growth

6 min read

KEY POINTS

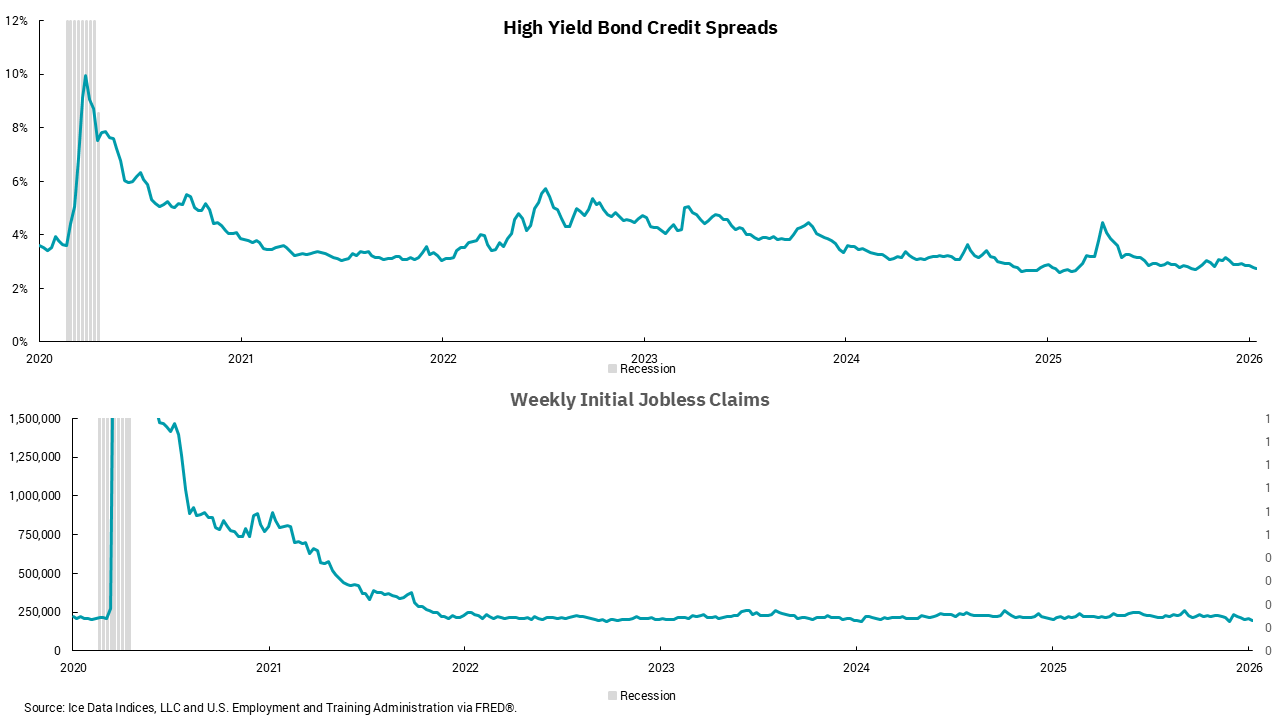

- Credit spreads and weekly jobless claims remain key indicators for validating or challenging the positive growth narrative.

- Geopolitical tensions and shifts toward a multipolar world present meaningful risks that could disrupt the base case outlook.

- Historically, positive January performance corporate incentives could fuel spending and investment, driving growth in 2026.

We had the opportunity to provide our 2026 outlook on Jan. 15. Joining me for the live panel discussion were our chief investment officer, Brian Henderson, and the president of our wholly owned investment subsidiary, Cavanal Hill, Matt Stephani. Visit our 2026 Market Outlook, for a written report of our views. A recording of the event will be posted there shortly.

Our base case for the economy and markets this year is one of more optimism than pessimism. We see a consumer supported by a stable-to strengthening job market, higher tax refunds, lower tax withholding and stable government spending. We also foresee higher capital expenditure (capex) across a broader part of the economy, driven by artificial intelligence (AI), infrastructure needs and aspects of the One Big Beautiful Bill Act (OBBBA) that incentivize business investment. Within this environment, we see good earnings growth and an inflationary environment that should allow the Federal Reserve to continue lowering rates, albeit slowly. As part of the wrap-up to the event, our moderator, Nasdaq’s global markets reporter Jill Malandrino, asked each of us the key thing we are watching as we move through 2026. As is normally the case, we each provided something that might put our optimistic base case at risk.

Brian highlighted geopolitical risks at the top of his mind—and why not? On top of the ongoing conflict in Ukraine, Middle East peace appears tenuous at best, and recent actions by the U.S. in Venezuela and comments around Greenland suggest the move towards a multipolar economic environment might not be smooth. It is hard to chart geopolitical risks, so for this week’s charts, I chose to represent the topics that Matt and I mentioned—credit spreads for me and weekly jobless claims for Matt.

In both cases, these are indicators that provide regular insight into key aspects of the economy. Credit spreads provide information on how corporate lenders view the repayment ability of corporate borrowers. In a growing economy, one would expect a high percentage of borrowers to repay their debt, and investors might require a narrower spread to compensate for the lower risk. The opposite is true if the outlook is for slowing, or even negative, economic growth. As more companies struggle to pay debts, investors require a higher spread to riskless Treasuries. Meanwhile, weekly jobless claims give us an update on the number of people who lose their jobs in any given week. Low weekly jobless claims numbers, as we have now, are an indication that companies are not trying cut costs by reducing employee levels.

The key will be whether we see a change in recent trends in these indicators. Higher credit spreads and higher weekly jobless claims would present information counter to our outlook—so far, though, this is not what we are seeing.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)