Jobs jump, inflation cools: a rare double surprise for the Fed

It’s still too early to signal ‘all clear’ on either Fed mandate

6 min read

KEY POINTS

- January’s employment report beat expectations with 130,000 new jobs and a decline in unemployment.

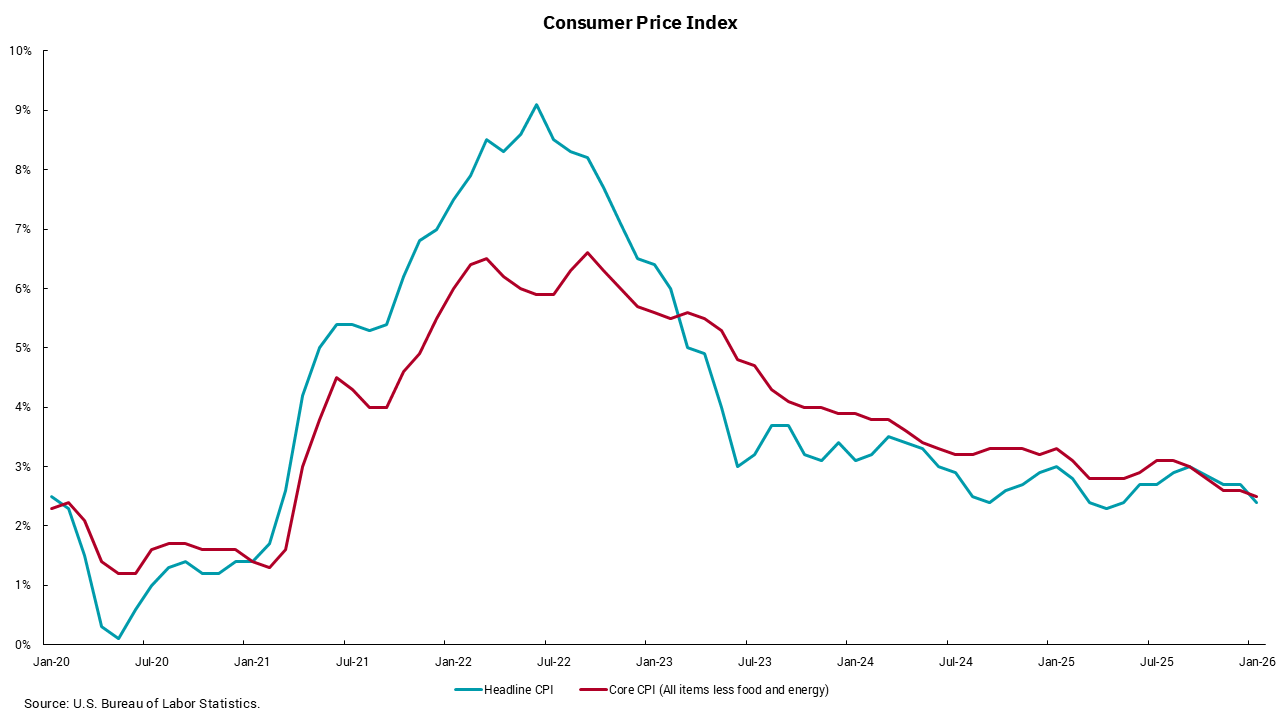

- Inflation also eased more than forecast that month, with core CPI rising just 2.5% year over year, the lowest since early 2021.

- While risks remain on both fronts, the broader economic picture is more optimistic than pessimistic.

Concerns and debate about politicizing the Federal Reserve aside, the real driving factors of interest rates and monetary policy are the labor market and inflation. They represent the two pillars of the Fed’s dual mandate, price stability and full employment. Last week, we got reports on both measures.

The January employment report from the Bureau of Labor Statistics (BLS) was delayed but reported on Wednesday. Likewise, the Consumer Price Index (CPI) report was delayed but reported on Friday. Going into these reports, the risks for employment seemed to be skewed to the downside—that is, higher risk of a weak report. Going into the CPI report, it seemed risks were skewed to the upside, a risk of somewhat higher inflation. In both cases, we received reports that were surprising in the opposite direction.

The jobs report showed higher-than-expected new job growth at 130,000, versus expectations of around 55,000, and a decline in the headline unemployment rate to 4.3%. The CPI report showed headline CPI at 0.2% below expectations of 0.3%, and core inflation at 0.3%. Looking at year-over year inflation, we now have headline inflation running at 2.4% and core inflation at 2.5%. Focusing on the more important measure (for Fed monetary policy, anyway) of core inflation, it rose 2.5% year-over-year, which is the lowest level since March 2021.

This is not to say we can sound the “all clear” on either of the Fed’s mandates at this time. Job growth has slowed dramatically over the last 12 months, and the BLS’ annual benchmark revision showed far fewer jobs created than first reported. Open jobs within the Job Openings and Labor Turnover Survey (JOLTS) have declined, layoff announcements, according to Challenger, Gray & Christmas, have risen to multi-year highs in January, and continuing claims show that those who are losing their jobs are finding it harder to get new work. Within the inflation data, this month’s lower numbers were helped by reduced food inflation and outright declines in energy costs. Within core inflation, lower new- and used-car prices and even auto insurance added to the continued moderation in shelter costs. Yet as consumers, we all know inflation is still an issue, as is the aggregate level of price increases since the onset of the pandemic. Even here, though, recent wage gains are now outpacing inflation, which, over time, should help budget-strapped consumers feel some relief.

There are always concerns and areas of worry within an economy as large, diverse and complex as ours. However, the aggregate mosaic of prices, employment, consumer spending and business investment keeps us more optimistic than pessimistic as we peer further into 2026. Stay with your plan.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)