Big tech isn’t driving returns anymore—at least, for now

As the mega-cap giants cool, the rest of the S&P 500 is driving gains

6 min read

KEY POINTS

- The “Mag 8” stocks have turned negative while the other S&P 500 companies—and especially the smallest 100—are delivering positive returns.

- Developed international equities and emerging market stocks are also positive.

- Broadening market strength supports a diversified approach as concentration risk in the S&P 500 remains elevated.

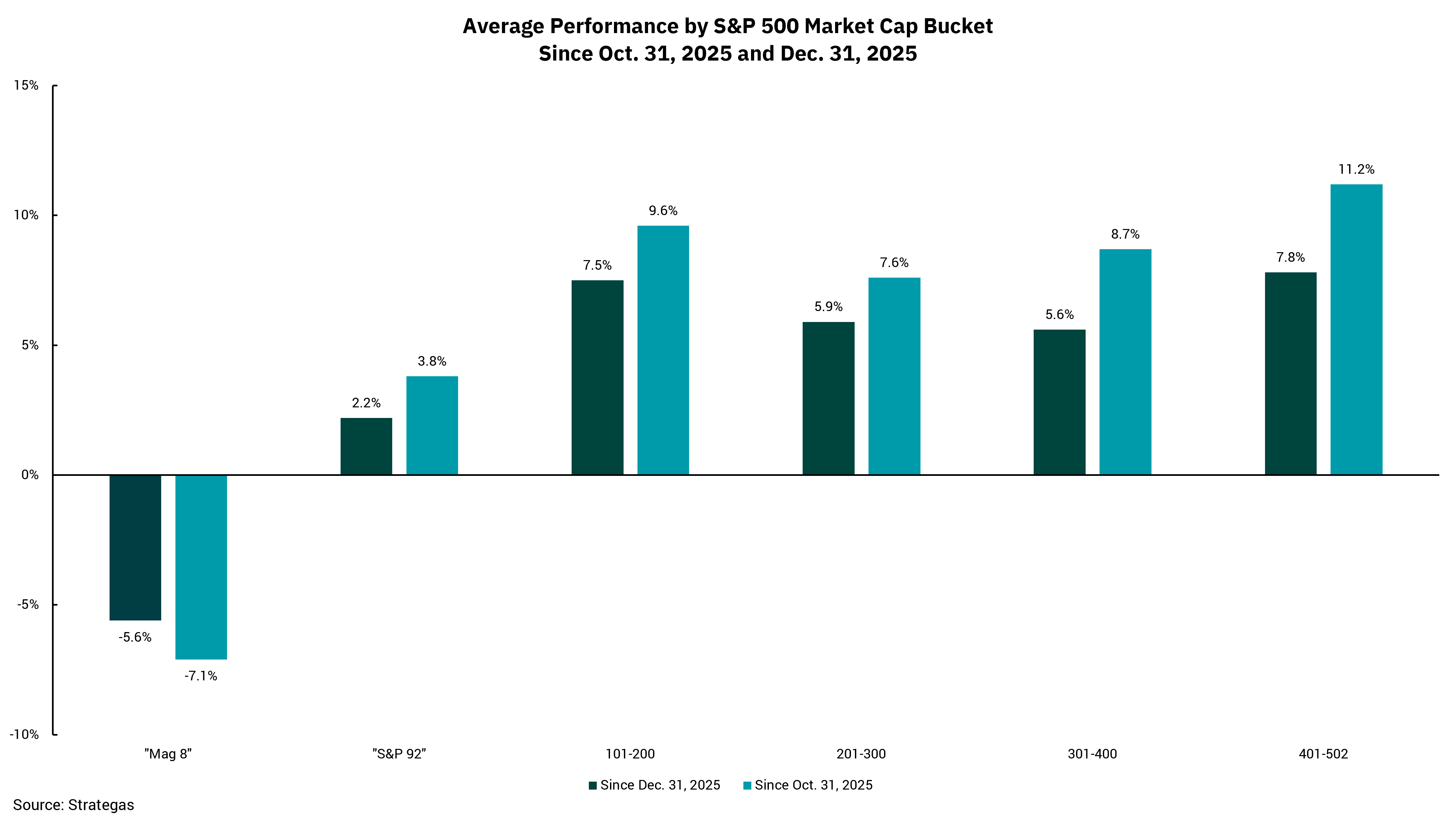

We have written extensively about the concentration of market capitalization, and performance, at the very top of the S&P 500 index. The top eight companies in the index represent a material portion of the its overall market cap, meaning the performance of the S&P 500 is being driven by a small number of companies. While not inherently bad per se, this concentration means the risk characteristics of this “diversified” index are different than times past. In short, the index is riskier.

One of the key parts of our 2026 outlook was the belief that economic strength would broaden beyond the top companies within the S&P 500. We included in this broadening thesis the idea that mid- and small-cap companies could see earnings growth accelerate, too. The idea then was that the performance of non-Mag 8 S&P 500 companies, along with mid- and small-cap companies, could be higher going forward, while the overall performance of the S&P 500 might languish. (We have added Broadcom (AVGO) to the more common Mag 7—which includes Apple, Microsoft, Amazon, Alphabet (Google), Tesla, Nvidia and Meta—to form a Mag 8.)

Our chart this week shows that this is what is happening so far this year. Through the close of business on Feb. 24, the overall S&P 500 index performance is less than 1%, basically flat. Yet, the performance of the Mag 8 is negative since Oct. 31 and year-end 2025. Moving to the right, we see that the remaining 492 stocks in the S&P 500 are positive in both time periods. The “smallest” 100 companies in the S&P 500 are up the most. This means that an “equal-weighted” index of the S&P 500 is outperforming the “capital-weighted” index we all follow.

While not shown in the chart, mid-cap and small-cap indexes are also positive year-to-date, with both up over 9%. We are also seeing a continuation of a trend that started last year, as developed international stocks are up about 8.5% and emerging market stocks are up over 11%, on a year-to-date basis.

We point this out to remind investors that a diversified approach means performance within overall portfolios can differ from the headlines. When investors were being paid to take the risk of just a few companies, a diversified approach lagged to some degree. However, we diversify to manage risk, and as the risk of the S&P 500 increased, we became even more committed to managing risk through diversification. The net result has been a period of relative outperformance over the last 12-18 months, and we remain committed to staying diversified going forward.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)