For markets, time is ticking on a de-escalation with Iran

Fears of stagflation—inflation coupled with slow growth—are reigniting

KEY POINTS

- Recent geopolitical shocks have followed a familiar “selloff-then-rebound” pattern, but the Iran conflict is proving to be more persistent and disruptive than past episodes.

- The shutdown of the Strait of Hormuz has triggered an energy price shock that simple policy adjustments can’t easily offset, raising the risk of prolonged inflation.

- If the conflict drags on, elevated energy costs and shifting Fed expectations could erode consumer-driven resilience and increase the risk of stagflation.

For roughly the past year, investors have leaned on a familiar playbook when major geopolitical headlines emerge: Markets sell off sharply at first, then rebound once the initial shock is delayed, softened, or partially reversed. This pattern has been especially common around policy announcements, where early fears often give way to pragmatic adjustments that calm markets. Not surprisingly, that dynamic surfaced again as tensions escalated in the Middle East, with many investors debating whether the latest conflict would follow the same short-lived trajectory.

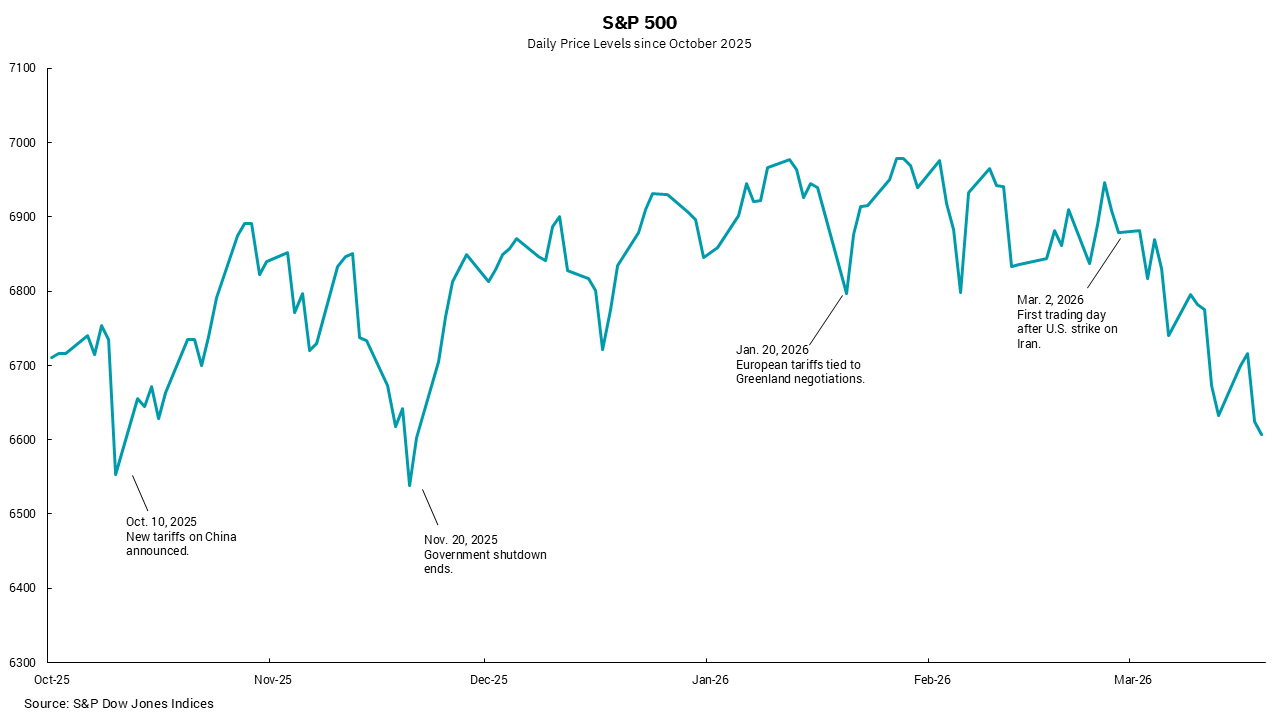

When the U.S. and Israel launched strikes against Iran on Feb. 28, early market reactions reflected a belief that the conflict would be short-lived and contained. Indeed, early investor behavior was optimistic: U.S. equity indexes saw only moderate declines, and some traders quickly rotated back into stocks to avoid missing an anticipated rebound. However, as the war entered its third week, Iran's actions proved more sustained and the U.S. is facing the possibility of prolonged commodity price inflation.

Many of these “selloff-then-rebound” episodes have been tied to trade and tariff disputes, where policy changes can be reversed relatively easily. This situation is different. The Iran conflict has led directly to an energy price shock due to the shutdown of the Strait of Hormuz, a development far harder to offset with simple policy adjustments. In response, the Trump administration has taken steps to ease supply pressures, including loosening restrictions on Venezuelan oil exports and waiving certain shipping rules to improve energy flows.

Consumer spending has thus far cushioned the U.S. economy through multiple recent shocks, but those buffers won’t last long if energy prices remain elevated. A prolonged conflict increases the risk of stagflation—that is, high inflation simultaneous with stagnant growth. Already, the Federal Reserve’s outlook has shifted: Prior to the Iran conflict, markets expected interest rate cuts by summer 2026, but with oil prices surging and inflation well above 2%, traders now anticipate potentially no rate cuts in 2026.

In effect, the U.S. economy is drawing on short-term stabilizers—in this case, household savings and policy flexibility—to manage the near-term impact of this shock. If the conflict resolves quickly, markets are likely to regain footing as geopolitical risk fades. If not, confidence built on early dip-buying assumptions could weaken, forcing tougher trade-offs. A swift de-escalation is becoming increasingly important; without it, investors may begin to price in a more challenging environment reminiscent of past inflationary regimes, with less room for policy support and fewer easy rebounds.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)