It's like the holiday guest that just won't leave. Heading into the new year, it's clear to see that inflation woes have overstayed their welcome.

"I think we should acknowledge that inflation has been more persistent than we thought," said Steve Wyett, chief investment strategist for BOK Financial®.

Inflation is the decrease in money's buying power—everyday goods and services cost more, so a dollar doesn't stretch as far and, therefore, has less buying power. And it's got people talking.

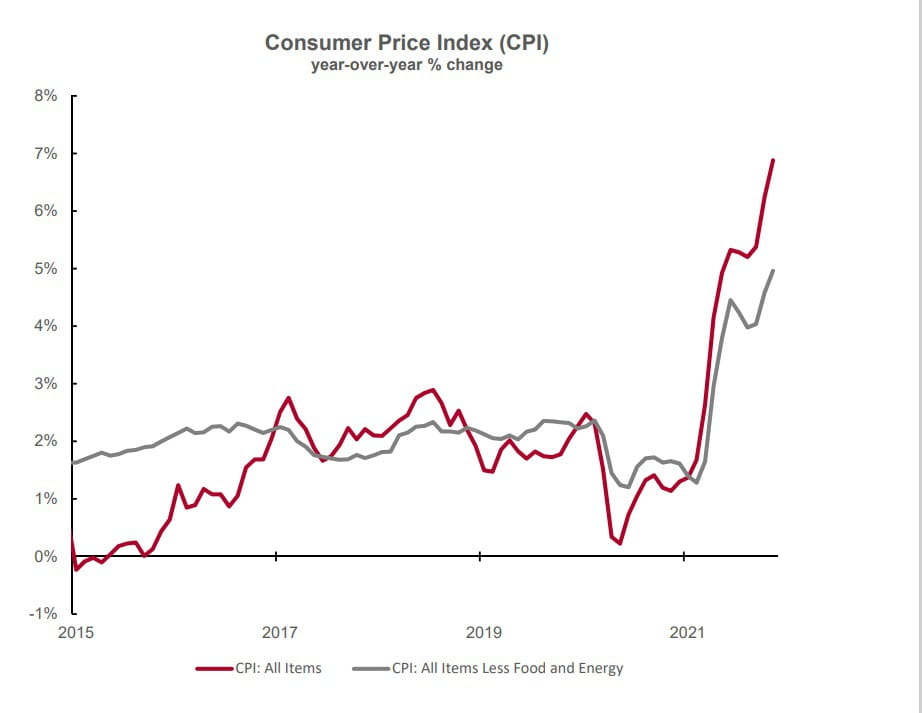

The Federal Reserve's goal is to keep the inflation rate at around 2%. But from November 2020 to November 2021, the Consumer Price Index (a metric that reflects the average price of food, clothing, housing, etc.) spiked 7% year over year—the fastest uptick in almost 40 years.

Chart Source: Federal Reserve Bank of St. Louis. Data as of November 30, 2021

Goods vs. services

The effects of inflation can be deep and widespread—from consumer behavior to the labor market, from kinks in the supply chain to the appetite for additional government stimulus.

"We are now seeing the economic impact of aggressive monetary policy and especially the impact of the multiple rounds of fiscal stimulus provided by Congress," Wyett said. "Because of things like stimulus checks, consumers had more money in their pockets to pay for goods and services in 2020 and 2021."

Those actions allowed demand from U.S. consumers to stay strong even while the pandemic limited the output capacity of the economy. "The actions of the Fed and Congress impacted both the supply and demand sides of the inflation equation," Wyett said.

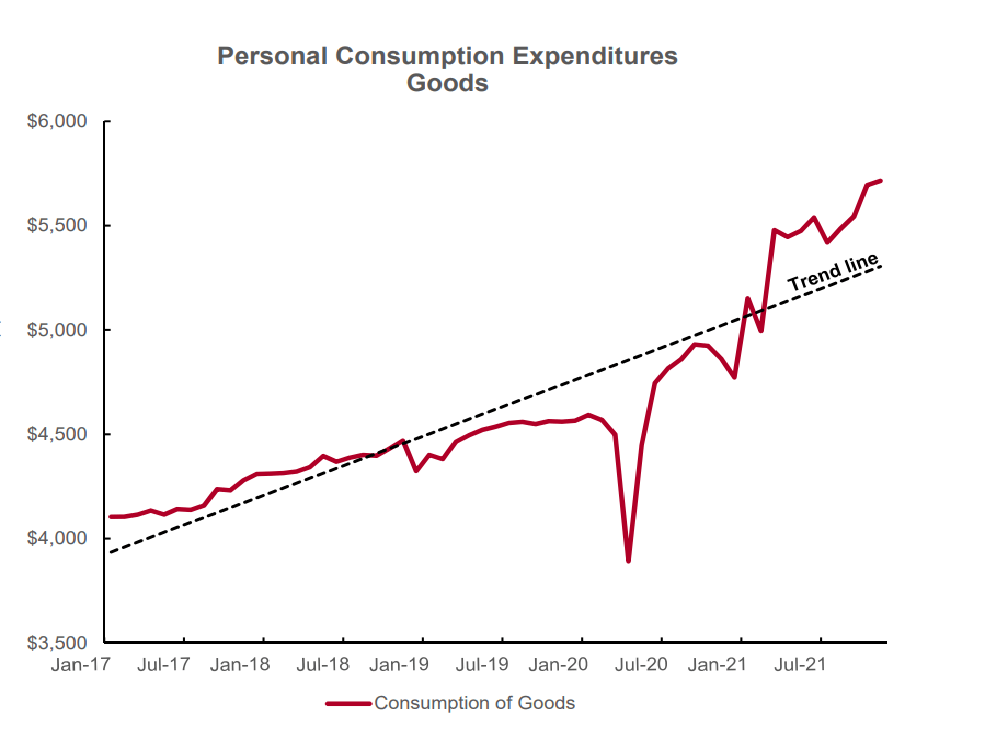

Data suggest the pandemic also influenced how consumers spent their money.

Chart Source: Federal Reserve Bank of St. Louis. Data as of November 30, 2021

"We could no longer eat out at restaurants or go to bars or casinos or take vacations, so we spent money on stuff," Wyett said. "Spending on goods within the economy surged over 20% above pre-pandemic levels, which helps explain some of the supply chain hiccups."

And while demand for goods rose, the pandemic disrupted employment in many areas. Manufacturers and retailers alike didn't have enough workers to meet the heightened level of demand, which led to ongoing supply chain disruptions.

But, Wyett doesn't expect that changed consumer behavior to last—at least not entirely. In 2022, he expects consumer spending to shift back from goods to services, and along with an improved labor market, should ease inflationary pressures.

"Our view is that over time the goods sector of the economy reverts back towards its longer-term level as the service side of the economy recovers, allowing inflation to subside."

In short, many think a cooling off is ahead.

A new-new normal

"But that's not to say it's a quick fix. Inflation is not going back to 2% or less anytime soon," Wyett said. "The normal we're going towards is not the normal we left behind. And our current reality isn't the new normal, either."

Wyett said a leveling out, and the creation of a new-new normal, is ahead.

"I think we're at or near a peak in demand and inflation for goods" he said. "Right now, the best way out of it is through it."